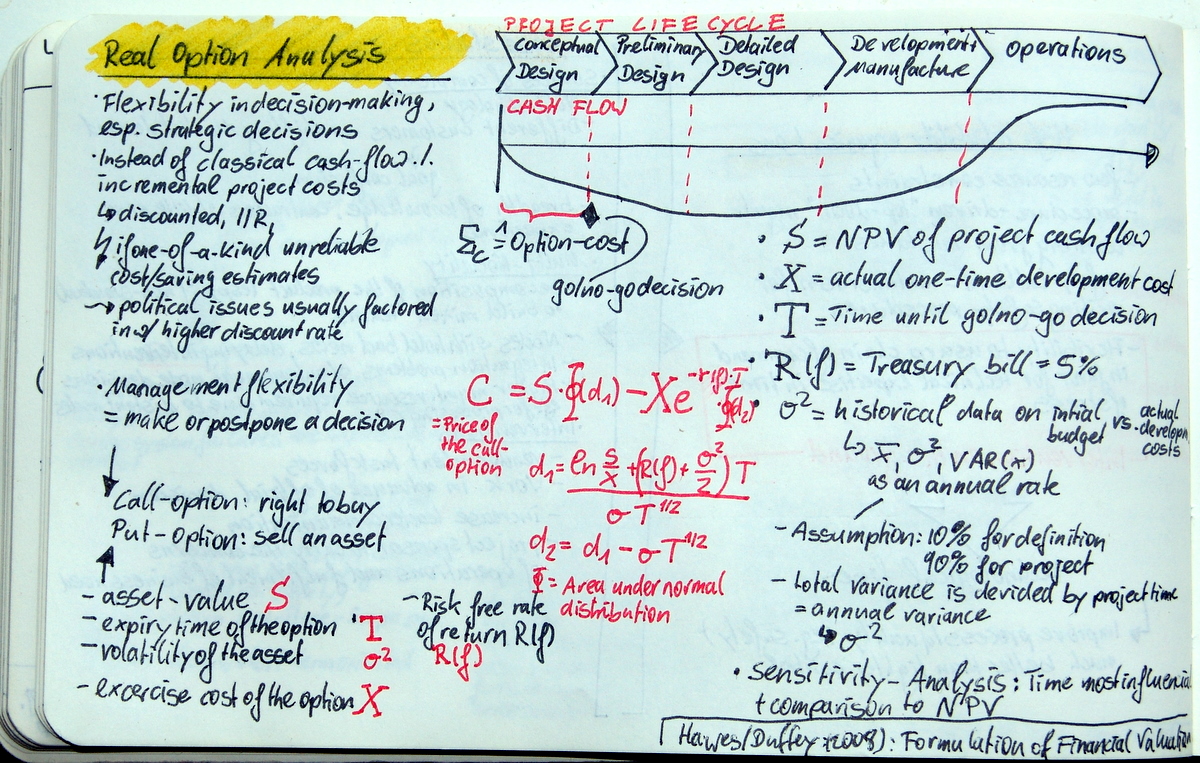

Hawes, W. Michael; Duffey, Michael R.: Formulation of Financial Valuation Methodologies for NASA’s Human Spaceflight Program; in: Journal of Project Management, Vol. 39 (2008), No. 1, pp. 85-94.

In this article Hawes & Duffey explore real option analysis as a financial management tool to evaluate projects. The basic idea behind that is management can make go/no-go decisions thus eliminating the downside variability of the value of the project. In short you can always kill a project gone bad of course with sinking some costs.

[Some might call again for Occam’s razor and argue that it is sufficient to model this into the cash flow, because for the option price you need a cash flow anyway. But the authors ]

To put the classical Black-Scholes formula to use the authors look for equivalents to the input variables. More specifically they analyse NASA’s space flight program and valuated projects in respect to their go/no-go decision after the conceptual design. The authors used as input variables

- NPV of project cash flow = Asset-value (S)

- Actual one-time development costs = Exercise cost of the option (X)

- Time until go/no-go decision = Expiry time of the option (T)

- 5% treasury bill rate of return = Risk-free rate of return (R(f))

- Historical data on initial budget estimate vs. actual development costs = Distribution of underlying (σ²)

Hawes & Duffey then compare the Black-Scholes pricing to the NPV and find that projects with higher volatility and longer time until decisions are higher priced than short-term decisions with less volatility (i.e. history of cost overruns).

I do find the managerial implications quite counter-intuitive. I modelled some Black-Scholes pricing for a real life project I worked on. My project had a NPV of 48 Mio. EUR but only an option price of 17 Mio EUR since the company had a history of cost overruns and a lot of front-loaded costs, in fact 70% of total expenditures would be spend before the go/no-go decision.

That is all very well and I can clearly see how that improves the decision making, but if I look into the sensitivity analysis the longer the time to decision and the higher the volatility the higher is my option’s price. This is where I do not fully understand the managerial implication. Given that a similar judgement rule to a decision based on NPV comparison, I would favour a project where I decide later and I would favour projects from a department with higher variability in costs, because this gives me a higher degree of flexibility and higher variability can yield a higher gain. Surely not!?!?